After 3-4 years of not visiting family, me and my family finally got a chance to travel to them in Kuala Lumper (KL) and Seremban in September 2022. And it was truly nice to meet them again – met my grandma who’s already 86, and 2 families of uncles and aunties and some of their kids.

What stood out to me during this time is chancing across personal regrets from a couple of friends and families – interestingly, they were similar:

regret going back to their home country in Malaysia, whatever the reasons then

I got a little reflective on this and how preventing regret is a big part of my psyche and adventuring in passive income, personal finance and financial independence.

Here are some takeaways:

You gotta choose the value you believe in.

I feel that that this is something that’s often ignored or overlooked, and not discussed enough.

Maybe it’s because it’s “in the air”, kinda airy-fairy, and maybe your parents or culturally you may not cover these kind of topics. I understand, I grew up in a stoic kind-of-grit-and-pivot as it comes. Which is an okay approach to float, but the problem with this is that it’s a coasting/floating without directions.

You need to choose which values (and principles) that are important to you and let these values help you make life and money decisions. It’d bring clarity and even happiness.

When you understand the values you choose, you can align with decisions you make. Let me give you an example of how I set values in my head and heart, when it comes to finance and money:

#1: My time and freedom is greater than money, so I dont want to keep actively working or being locked into a situation long term for money. My money needs to be generated passively and work harder for me.

#2: I dont want bloody or shady money. My money that is made needs to be made with the regular work and through investments that are clean. I do not want to make dirty money. This leaves plenty of money on the table but I sleep well and I am comfortable to meet my Maker.

These 2 money values drives the way I do business and spend my money, so it’s commonplace to see me prioritize decisions:

- that make money for me passively, such as being pre-occupied with dividend stock investing and eventual property investing

- decrease taking on expense-generating activities unless its a true need, such as expensive cars and watches and phones, which bring me zero joy

- teaching my kids about business and money and ethics

See, there’s a lot of societal pressures (be it family, friends, advertisements) which can be huge – when you don’t know or hadnt chosen your values, you can be easily affected and swayed. That’s why you need to know what’s important to you.

Of course it comes with sacrifices – I have to follow my values of not buying those swanky cars even if I can afford them. It just doesnt make sense to me. My friends who want to migrate will have to live with the pains and perhaps some loneliness; especially seeing their loved ones in medical conditions or even passing on, without being there by their side.

You’ve gotta know and decide what’s important to you, be it for money, life, love, career – define them clearly and these value will help you avoid big regrets down the road later.

Plan in advance and execute consistently based on the values you believe in.

This is a continuationof the values point I shared above.

It’s one thing to know and choose the values you prefer; it’s an entirely different thing to plan in advance and execute consistently based on the values you say you believe in.

Talking and thinking isn’t enough, you gotta do what you say and keep doing UNTIL it’s done.

Again, I will use my example of my financial and money values:

#1: My time and freedom is greater than money, so I dont want to keep actively working or being locked into a situation long term for money. My money needs to be generated passively and work harder for me.

#2: I dont want bloody or shady money. My money that is made needs to be made with the regular work and through investments that are clean. I do not want to make dirty money. This leaves plenty of money on the table but I sleep well and I am comfortable to meet my Maker.

For me to live the passive income lifestyle where my investments will pay for my lifestyles and expenses, I will definitely need much more than I can invest right now.

From a very conservative standpoint, say I want to have $10,000 to spend every single money so that I dont have to worry about money, assuming a 5% return on investment, that would mean I will need $2,400,000 (This number is derived by annual amount ($10,000 x 12 = $120,000) divided by 5%).

Two problems:

- I dont have that large sum of money lying around: I need to think of how to break that down into bite-size-chunks where I need to earn and invest X amount over a Y period of time

- I need to consider the possibility of adding a buffer, say 20-50%, in case things change down the road (who knows right?)

How to amass $2,400,000 in the least time possible

Perhaps, I can consider moving to a cheaper cost of living space. Maybe a cheaper country, or a cut down from $10,000 to $5,000 (this will decrease the amount to a much more easily $1,200,000).

If that can’t be done or I’m not willing to, then the next thing if I want speed, then I need to answer this question:

How much can I earn and invest per month/year?

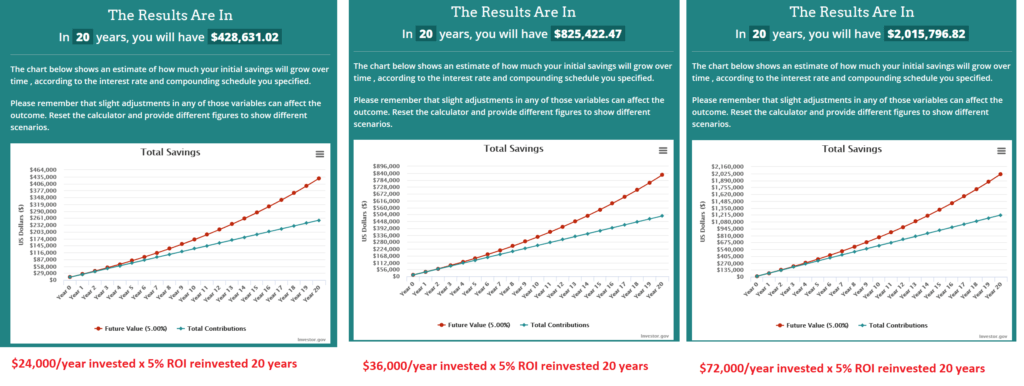

The more I can invest, naturally the timeline decreases. Here, let me show you.

The more money you can invest, the faster you can accumulate (kinda straightforward).

How can you improve on this?

- Earn + save + invest more. This is the easiest in my opinion and is the #1 focus of mine, because I enjoy business so much. Why? Because business can grow. This year I may have $50K profits, but next year with improvements, we may earn $75K, and the extra $25K can be invested. The year after that maybe more and so on so forth. Business also can be sold for a sweet multiple that can accelerate my personal finance amount target too (I sold my first business for a sweet 7 figure deal after hustling like madlad for 10+ years).

- More time (I dont like this because time is the only resource we cannot replace or earn back; but this will work great for someone really young eg your kids/family/newgrads) but not suitable for me who’s 40 at this time of writing.

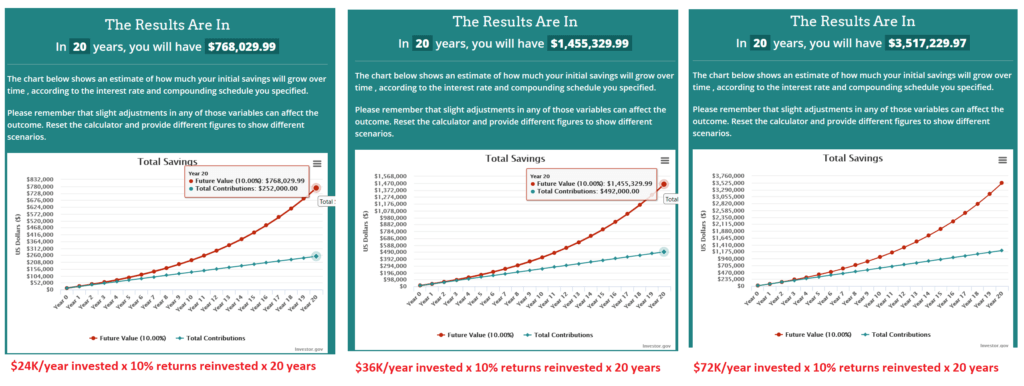

- Improve on your ability to research and invest. The calculations above are based on 5% returns. What if you can find something that can give you 10% per year? That changes everything. Let me show you:

Look at the difference – it’s massive. 2% vs 3% vs 5% vs 7.5% vs 10% etc can have startling differences. But investing can be hard and choosing the right steps can be hard, and I dont want to monitor the market too much or have too much volatility.

I take the approach of

- earn more building and growing business which pays for my living expenses

- dont spend unnecessarily

- invest as much as possible into relatively stable dividend stocks, investment properties and even vanguard (not dividends, but been 8-9% last 10 years)

That’s it.

Regardless, can you be patient for 20 years? It may be earlier if my business profits grows exponentially and I can invest more and more.

I can and I will, to prevent as much regrets as possible.

Resisting influece, the joneses and lifestyle creep

You may have come a long way from being that broke student living off instant noodles. I know and remember those days.

Maybe nowadays you earn a lot more, and can now afford to enjoy a much more expensive lifestyle because

- you worked hard for it

- you deserve it

- you wanna catch up on lost time

These are what I call “lifestyle creep”, and they’re like addictive feel-good-drugs that does make you feel powerful and good…but only for a while. The more you earn, the more you spend.

- Maybe your neighbour bought a swanky 4 wheel drive and you like it and thinking of buying a 2nd or 3rd car

- Or your parents are bugging you to refinance their home for them or telling you to buy a bigger house

- Maybe your close friends are planning to go on an expensive trip

- Or your spouse wants an expensive gift

- etc

And then after, nothing changes. Sure, you have more expenses and things to pay for. If anything, your bank account is smaller, and you’re further from your passive income lifestyle.

The longer you can live on a small budget with minimal expenses, the more you can save and invest — and the easier it will be to have more choice, freedom, and flexibility in the future.

Yes, it’s sometimes tough to cut back when you’re used to spending more or to a certain lifestyle. By practicing more frugal habits now, you can invest more and have more than enough to “play” with the extras later.

Save and invest as early as possible

When you’re young (20s or 30s), you have a big advantage that older people dont have: time.

Time is a very powerful tool that helps to compound your money, and the longer time you have, the more it can compound your investment returns and be increasingly profitable. I’ve shared this earlier so I wont go too much into this.

- Person A who invests $1K/month upon graduation at 22 years old, and continues all the way till they retire at 62 (total 40 years) with 5% returns will have $1,449,597.29

- Person B who invests $1K/month for 10 years with 5% returns will have $150,934.71

See the big difference when time is involved? Time plays a very big role especially when it comes to personal finance and financial independence.

Regret prevention

After hearing the personal stories of the regrets, I am doubling down on my efforts to

- build even more passive income streams and portfolio

- carving out more time to spend with people I care about including praying/time with God

I dont want to regret when I’m old, because when I’m old, I cant catch up; so this means I need to anticipate as much as I can to go in the direction of where and who I want to be in 10++ years time.