WHAT IS PASSIVE INCOME LIFESTYLE?

I didn’t realize it at the time, but Passive Income Lifestyle and passive income has always been an important topic and focus in my life, and is #3 of all I do (#1 and #2 and God and family respectively). The thrill of getting passive and dividend income still makes me excited till today =D

I shared in other articles in NigelChua that I won’t deep-dive on nitty-gritty evaluations of stock and investments, because I’m not wired that way – I focus much much more on philosophy, strategy, systems, sustainability, scalability, leadership, decision making and transformation – more high-level, concepts and systems perspective.

This article covers more about FIRE, what it is, how to get there etc.

FIRST OF ALL, WHAT IS PASSIVE INCOME LIFESTYLE?

The acronym FIRE, stands for: financial dependence and retiring early.

In simple terms, it means that your monthly expenses are covered for my the passive and dividend incomes from your investments, and you can scale down work (or not work at all), and explore other interests or spending time with family or worthy cause ie retiring early without worrying about money.

WHAT DOES PASSIVE INCOME LIFESTYLE COVER?

It needs to cover all expenses for the next 30-50+ years (to me, until I die la), and have buffer for unexpected costs and extra for spending. So to me, it needs to have forever continuity lol, hence I aim to over-save/over-compensate (more on this below).

WHY PASSIVE INCOME LIFESTYLE?

Hmm. A few words, but it generally means: flexibility, options and freedom.

To be, being unshackled, unbound, free to move and not worrying about money is a very liberating feeling and thing. It means to be able to:

- choose what you want to do

- choose where you want to be

- choose who you want to spend time with

- choose what interests you

- choose family/volunteer/etc

HMM. CAN EVERYONE DO IT? SEEMS LIKE ONLY PEOPLE WITH A LOT OF DISPOSABLE INCOME CAN DO IT.

Yes and no.

Everyone can do it, and yes, it does seem like people with lots of disposable income has it easier (it’s true cos when you earn more, you have/can* save more).

*Caveat: IF you save more. More often than not, people who earn more, extend and grow their spending too ie their spending increases symmetrically with their earning, and they have bigger toys and expenses to play with. If they can earn a lot and save a lot, that’s the sweet spot for FIRE!

It’s not just how much you earn, but the contingent is how much you can save and invest month after month into stable investment/dividend stocks.

FIRE is for everyone, and yes, it’s easier for

- those who can save more

- those who can earn more

- those who spend less or have less fixed expenses

- those who can diligently invest and reinvest dividends into more dividend-paying stocks/investments.

Generally those four points lol to FIRE. It’s a very good practice and philosophy anyway, with great outcome once you achieve FIRE (see above).

EH, IS THE MATHS SOUND?

Our basis of Passive Income Lifestyle is based on:

- having 25X our annual spending into an investment nest (which is invested into cash/dividend-paying dividend stocks and/or investments)

- 4% withdrawal rate

There is this study in 1998, called Trinity Study, which looked at retirement portfolios which consists of stocks and bonds with a withdrawal rate of 4% withdrawal rate…survived 95% of all retirement periods from 1926-2017!

This basically means that if your monthly expenses is $2000, hence your annual expenses = $2000 x 12 months = $24000, means that you need $24000 x 25 = $600K as your investment nest.

Assuming you invest in dividend stocks/portfolio that pays you 4% per year, that’d mean 4% of $600K = $24K per year = $2000 per month.

That’s it. Of course, you job will then be to:

- keep your monthly expenses below $2000

- reinvest any surplus/unused dividends

SOME NUMBERS

So if you can/need to live within 4% annual withdrawal rate, then your investment nest is the inverse of that rate ie 4% = 4/100, hence inverse = 100/4 = 25X of your estimated annual living expenses.

If you need to live within 4%, then the inverse of that is that – your investment nest needs to be 25x your projected annual living expenses.

Example:

- If your month expenses is $2000, hence annual expenses is $24000, so your investment nest is 25X of your yearly expense = $600K

- If your month expenses is $5000, hence annual expenses is $60K, so your investment nest is 25X of your yearly expense = $1.5M

- If your month expenses is $10K, hence annual expenses is $120K, so your investment nest is 25X of your yearly expense = $3M

PASSIVE INCOME LIFESTYLE RULES

- Spend less than you earn = more savings/excess

- Invest as much/all your excess in dividend/passive income stocks or investments

- The more you can earn, save and invest is directly related to how fast you can reach FIRE

…AND THE 1ST MOST IMPORTANT RULE:

Barring your earning rate, it’s how much you can save and invest into dividend paying investments that will bring you sustainably closer to your FIRE timeline and goal.

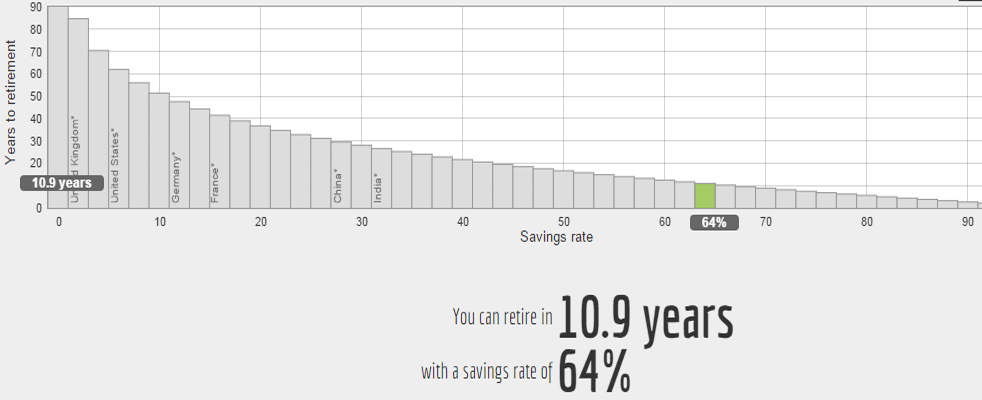

Of course, the higher savings rate, the better (we’re talking north of 60-75%).

In fact if you refer to the graph below (from Mr Money Mustache), if you can save 64% of your income and invest into 4% dividend paying investments and reinvest the dividends, you can retire full Passive Income Lifestyle in less than 11 years.

Yes, 11 years.

Credit: Mr.MoneyMustache

Most people are shocked with 64%, and think that 10-20+% savings is good enough, but consider this: if you save 30% and invest into 4% annual returns, you can retire in 30 years.

What more if you save 10-20%?

It’d be a lot more time required.

So…

EH, SO ALL I NEED TO DO IS JUST SAVE RIGHT?

Aggressive saving is the first step – culling unnecessary expenses and optimizing spending is the basic first step. The next is if you cannot save more, then you need to earn more to invest.

The next step is then to invest:

- diligently

- consistently

- responsibly

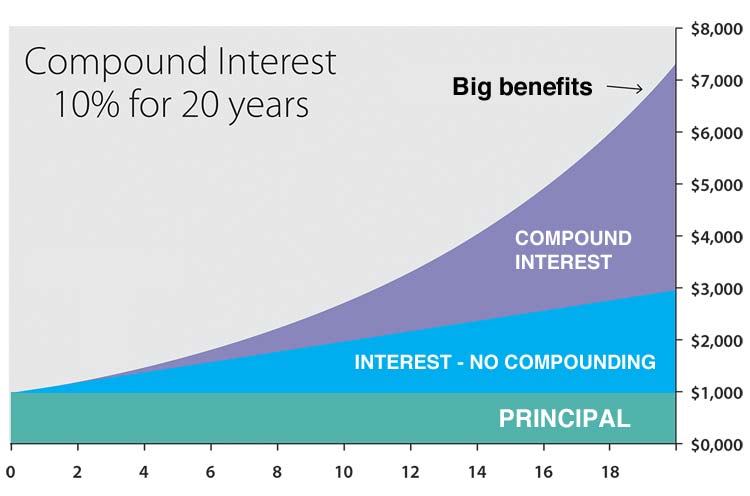

…to get Compounding Interest (what a beautiful word, wipes tears from eyes) – compounding interest is accelerating and growing your savings/investments.

Give you a simple analogy: if you save $1000 per month x 12 months x 20 years, you would have saved…$240K right?

No, that’s not enough. I expect every dollar to work hard for me to birth more cents and dollars (insert evil laugh here lol). Let’s use the graph below to illustrate:

COMPOUND INTEREST, A SHEER JOY

Credit: https://www.thecalculatorsite.com

Assuming 10% interests per year, with $1000 invested per month, to compound means to take the interest and reinvest, so it’d look like this:

- Year 01: $13200 (ie $12000 plus 10%)

- Year 02: $27720.00 (ie $13200 + $12000 plus 10%)

- Year 03: $43692.00 (ie $27720 + $12000 plus 10%)

- Year 10: $210374.00

- Year 20: $756029.99

So, instead of having $240K after 20 years as mentioned earlier, with 10% return and it being reinvested, you end up with $756K. Like what on earth is this magic?

It ain’t magic baby – just maths and compounding interests.

Most people use compounding interest in a bad bad way (think paying bare minimum off credit cards or loans with interests), so doing this instead will use compounding in a powerful way – in your benefit.

BUT I DON’T KNOW WHERE TO INVEST

I don’t tend to want to advice which specific investments to investment/speculate in, so generally rule of thumb: do not gamble or speculate.

To retire early, you need stuff that is proven and has been around since 5-10++++ years (ideally 20-30+ years) with data showing it’s stable and reliable.

After all, if you want to retire early without worry about money coming in, you need reliable investments right?

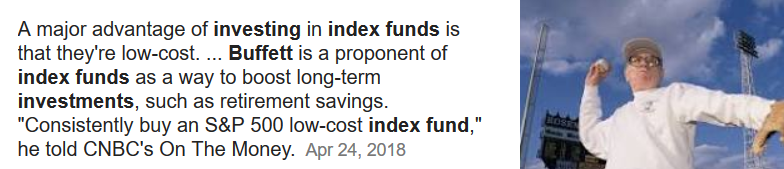

So the easiest and probably the safest is low-low-low fee investments like index funds, which is also recommended by well-known Warren Buffett.

By investing in index funds, it doesn’t require you to have any technical knowledge or “gaming/timing the market” – you basically invest into a fund that aggregate the performance of the top companies in the country that reflects the general economy of the country.

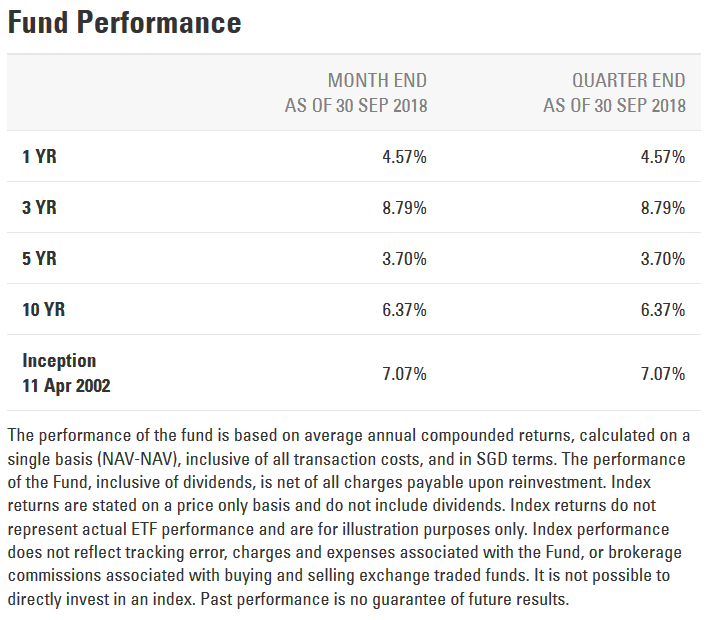

If you’re talking about Singapore, then it’s the STI. If you take a peek at SPDR STI ETF website, you can see that it’s been about 7+% return since inception.

Technically if you are averaging 7% and you’re only withdrawing 4%, you have a good 3% that is considered still working for you day-in-day-out.

However on a real-life basis, the actual dividends from STI ETF ranges from 2.6-3+% in actuality (I believe the aggregate 7% includes capital appreciation, and wanted to bring this up).

Of course you can choose to buy other investments such as individual stock picking, land banking, real estate etc but after trying my hands on a few different types, I still prefer dividend stocks because it’s easy (it’s liquid; dividends are non-taxed and wired automatically into my bank account with little to do compared to real estate investing etc) and hence it doesn’t distract me from my core functions such as writing, business, fathering, spending time with loved ones.

KEY TO PASSIVE INCOME LIFESTYLE

The simple and the most common way of FIRE is essentially a combination of minimalism, DIY, anti-consumerism, lots of patience.

The maths here is basically the less you need to live with/on, the less you need saved/invested and the faster you can reach your FIRE goal.

We actually dont need to spend that much on stuff actually (my opinion) – simplicity and frugality can be quite satisfying.

- I don’t need or want to work extra 20 hours so I can bring my wife and kids to a nicer place that ends in 1.5 hours or a fancy car/bag/clothes

- I don’t need or want to work extra 20+ hours per week so I can buy a larger space

- I don’t need or want to work extra hours just so that I can buy more shit. I don’t mind working/investing and budgeting for important stuff like insurance, food, travels etc but I don’t want to spend my life working to pay for stuff that in the end I can’t enjoy or be with people I love.

Like, what’s the point of working 20-40 hours to pay for a larger house where I can’t enjoy or can’t be with my wife or kids…so I can pay for the larger house?

If you can cut unnecessary Decadent Expenses, you will cut your required savings/time/required amount to reach your Passive Income Lifestyle.

- If you cut expenses by $100 a month ie cut $1200 a year, you can shave off $30K from your investment nest required

- If you cut expenses by $500 a month ie cut $600 a year, you can shave off $150K from your investment nest required

- If you cut expenses by $1000 a month ie cut $12K a year, you can shave off $300K from your investment nest required

How much time would that save you in years?

MY TWIST TO THE USUAL FIRE: THE PASSIVE INCOME LIFESTYLE

My FIRE+Passive Income Lifestyle approach is the same as above but with a little twist:

- 25X annual expenses isn’t enough for me – I prefer more buffer so a good 30X+ of my annual spending will be better for more buffer and unexpected events

- I want to be free but I want more flexibility in terms of being able to buy/spend should I wish it, so back to point #1 just above – 30X+ will be my target.

- I want to accelerate my 30X accumulation AND build a meaningful lifestyle business, so I will focus on entrepreneurship (have been an entrepreneur since 2008 anyway), where I can not only earn well, but there is no ceiling to what I can earn and more importantly, give back and effect change such as creating jobs etc.

BEWARE THE HIDDEN AND SNEAKY MONEY GRUBBERS

Too many of these around.

From the smallish ones like:

- that “small” snack (bread, fried stuff, sweets) which can go from $1.50 to $5 per order

- that “smallish” bubble tea/coffee/tea which can costs $3.50 to $7+ per order

- that weekly decadent splurge that can cost anything from $50-$1000+ per order

Say we take an average per month:

- snacks ~ 10x per week of $3 x 4 weeks = $120 per month

- drink ~ 5x per week of $5 x 4 weeks = $100 per month

- splurge ~ 1x per week of $200 x 4 weeks = $800 per month

That’s $1020 per month or $12240 per year.

Invest that with 4% return with compounding over 20 years = $379063.03. The other way to look at this is that every $1020 expense you have increases your nest size requirement by $300K+ per year.

(Imagine any other money suckers).

AIN’T THAT A MISERABLE WAY TO LIVE, NIGEL?

Please, what I urge is to ruthlessly cut out stuff that:

- do not benefit your health

- you don’t even like but do “cos people do it” or “to impress someone who don’t care”

Those kind of expenses – kill them. Save those and take the savings to invest in dividend stocks that pay you dividends to spend on things you care about – including bubble tea.

100% guilt free.

FIRE is not just about being frugal nor being cheap – it’s about curating and choosing a conscious lifestyle of what that you care about. I can’t live cheap nor be miserable, unless it’s bad habits that I need to break (eg you don’t need retail therapy to be happy).

It’s also being mindful of what you want to do with your money today, and building a financially independent and retiring early for a near future. You’d be surprised, that FIRE lifestyle isn’t about depriving yourself of a pleasure, instead, it’s replacing it with something better, healthier, happier.

FINE, FINE – HOW DO I START MY PASSIVE INCOME LIFESTYLE JOURNEY?

Great.

1. First you need to look and understand your own personal math to retire comfortably.

2. Then, track your expenses. Find out the stuff that you don’t really care about, and ruthless optimize and remove them. All these expense savings/saved – they go into investment fund.

3. Next, optimize your savings rate – again, look at what you spend on. If you can, cull the Decadent Splurges (for now) and focus on Basic Expenses (basic shelter, basic food, non fancy lifestyle). All these savings – they go into investment fund.

4. Then, take all those cost savings and savings that went into the investment fund – pump them regularly into safe, defensive and reliably-paying dividend stocks or index funds. Reinvest the dividends or you can split the dividends 50% for reinvestment and the other 50% on anything you want to, guilt free. (Of course if you reinvest 100% you will reach FIRE goal faster, but this is your call and freedom).

5. Rinse and repeat until you hit your FIRE goal.

That’s the easy (but boring) part.

The fun part comes when you hit your FIRE goal and/or finding a side hustle that you really love or that brings deep meaning to you.